Dr. Antonia Dimou[1]

Introduction

The discovery of natural gas resources in the East Mediterranean promise important benefits of energy security and economic gains. A 2010 US geological survey showed that the Levantine basin - offshore Israel, Gaza, Lebanon, Syria and Cyprus - could hold as much as 120 trillion cubic feet, thus securing supply of energy not only for the countries of the region but also for Europe.

As this paper will show, regional countries are currently at various stages of exploration and development which are however fraught by political risks and policy dilemmas. Thus cooperation, conflict resolution and the creation of interdependency structures are prerequisites to unlock the potential of the region and safeguard the unimpeded flow of future gas production.

Israel as a Catalyst for Regional Energy Cooperation

The gas discoveries have strengthened Israel’s energy security, and decidedly contribute to the reduction of Israel’s dependence on foreign energy. They also provide the promise of economic advantages given that natural gas

supplies direct income to the state treasury as a result of royalties and taxes paid by gas suppliers.

Israel is a leading country for regional energy cooperation because the preparations to extract gas from its major fields, Leviathan and Tamar, are already at advanced stages. For the record, Tamar was the largest deepwater natural gas discovery in the world in 2009 and sales from the field began in 2013, just only four years from discovery. Leviathan was discovered in December 2010 and represents the largest exploration success, with gross mean resources of 22 Tcf of natural gas[2].

Following Israel’s High Court of Justice approval of a government decision to export 40 percent of the country’s offshore gas discoveries, Israel looks into a combination of export options on the basis that gas is a game changer stressing the inevitability between macroeconomics and geopolitics. It is in this context, that priority is given to Jordan as disruptions of energy imports from Egypt have impacted the Kingdom’s public budget and fiscal space for broader development goals. The sale of Israeli gas to Jordan falls within Amman’s broad strategy for transformational change in energy supply, including a diversification of natural gas imports from alternative sources in the region.

Noble Energy, a heavy foreign investor in Israel’s fields, has signed a contract worth $500 million to supply 66 billion cubic feet of gas from Israel’s Tamar field to Jordan’s Arab Potash and its affiliate Jordan Bromine. Leviathan partners Noble and Delek have also signed a non-binding letter of intent with Jordan’s National Power Electric, which will act as buyer of the gas, to supply 1.6tn cubic feet over a fifteen-year period[3]. Other investigated projects focus on the construction of a 25-kilometer pipeline that would connect northern Israel to northern Jordan, facilitating the supply of natural gas to major Jordanian manufacturing plants.

It is acknowledged that infrastructure partnerships between Israel and Jordan can provide real incentives to normalize relations, given that the supply of cheap and reliable energy will bolster the kingdom’s economy and that Leviathan partners’ export earnings will increase.

Figure 1: Israel’s export options

An additional option for the monetization of Israeli gas centers on Egypt, which suffers from domestic gas shortages due to export obligations and a growing population. Cairo’s political instability, heavy regulations, and ceiling on onshore prices have transformed over the years the Arab country from a gas exporter into a heavy energy importer. Although Egypt’s total proven reserves are approximately 2.2 trillion cubic meters, its production levels and reserves have not improved despite technological breakthroughs and massive capital expenditures, leaving two major LNG facilities in Damietta and Idku virtually idle.

For this reason, Israel’s energy policy vis-a-vis Egypt has a dual dimension; on the one side, it centers on the sale of gas from Leviathan and Tamar fields, and on the other side, it looks into using Egypt’s LNG facilities as export terminals to reach markets like Europe and Asia.

Thus, pipelines from Israel’s gas reserves to Egypt for liquefaction and re-export has become a real choice, taking into account the close distance between the Egyptian and Israeli coasts. The option for the transport of Israeli gas to Egypt is either through reversing the flow in the Egyptian export pipeline that crosses Sinai or the construction of a new undersea pipeline and it is esteemed as viable not only because of the royalties and revenues Israel will collect but also because of the potential positive impact on Egypt-Israel bilateral relations.

Already, partners of Israel’s Tamar field have signed a non-binding letter of intent to export up to 2.5 trillion cubic feet of gas over 15 years via the Damietta LNG plant in Egypt operated by Union Fenosa Gas, a joint venture between Spain’s Gas Natural and Italy’s ENI.[4] Similarly, Leviathan partners reached a preliminary agreement with British Gas (BG), a British oil and gas company, to negotiate a deal to export gas to BG’s liquefied natural gas plant in Idku (northern Egypt) via a new undersea pipeline.

To move one step further, the recent decision of the Israeli energy ministry to grant its first formal approval for the export of gas from the Tamar field to Egypt's Dolphinus Holdings, while still hinging on regulatory and other bureaucratic approvals, paves the way for regional cooperation in the gas sector that can eventually include countries like Jordan and Cyprus. Notably however, gas import talks have ceased due to the recent rule of the International Chamber of Commerce according to which Egypt must compensate with 2 billion dollars Israel for the repeated halting of gas supplies via the El-Arish-Ashkelon pipeline. According to energy officials, it is important for talks to restart on the precondition that both countries agree on compensation reduction or even complete compensation elimination in lieu of an import agreement with Israel that will definitely revive the Israeli gas export infrastructure.

Another export option to immediate neighbors includes a subsea pipeline from Israel’s Leviathan field to Turkey, but this is currently considered politically non-viable. There is widespread consensus in Israel that without a political reconciliation between the two countries, any advancement of an export agreement remains remote. Specifically, even though the project is tempting to private companies because the construction of the 480 kilometer pipeline would be cheap[5], Israel appears cautious in entrusting its most precious resource to Islamic Turkey because of the likelihood that the Turkish leadership waves the card of gas in the face of Israel in times of political crises thus rendering Israel hostage to Turkey.

Reservations are also expressed regarding financial security in any future framework energy agreement between Israel and Turkey, with suggestions centering on that financial security can be provided by a third party such as the U.S. Overseas Private Investment Corporation, the U.S. Export-Import Bank, or the German Euler Hermes company.

When it comes to the Israel-Palestine front, discussions revolve around the Palestinian control of the West Bank’s energy industry with the enforcement of a deal signed between Leviathan partners and the Palestine Power Generation Company, which foresees the purchase of $1.2 billion worth of Israeli natural gas over a 20-year period.[6] For the gas to be shipped to the Palestinian power plant in Jenin, which will permit Palestinians to produce their own electricity and create jobs in the West Bank, construction of a 10-kilometer gas pipeline from Northern Israel has to materialize. But it is still pending because of lack of political will.

A Note on Israel’s Anti-trust Challenge

The regulatory uncertainty in Israel has stalled the development of the Leviathan field and thrown into limbo gas export agreements with Jordan and Egypt since December 2014 when the Israeli Anti-trust Authority commissioner issued a recommendation for investing companies to divest from the Tamar and Leviathan fields.[7] The reason is that the Israeli regulatory framework foresees the establishment of a competitive gas market and upon this the anti-trust commissioner has the authority to block any trade agreement perceived as violating competition laws.

In an effort to overcome regulatory obstacles and reignite a number of preliminary agreements to export Israeli gas to Jordan and Egypt, the Israeli government approved a revised gas agreement in August 2015 with the partners of Tamar and Leviathan fields.[8] The revised gas agreement has aimed to manage the speedy development of the gas fields and create competition, setting aside anti-trust regulations and conflicting state decisions on issues, such as taxation and prices.

Under the agreement terms, in a frame of six years, Israel’s Delek group will sell its holdings in the Tamar, Tanin and Karish fields, and US Noble Energy will reduce its holdings in Tamar to no more than 25 percent. In addition, the agreement contains a “stability” clause that binds the government for the next fifteen years to unchanged regulations pertaining to the structural and financial facets of the Israeli gas industry. The agreement also foresees the implementation of a deal to export gas from Tamar field to the Egyptian liquefaction plant of Idku for re-export to Europe, and the introduction of a timetable for the development of the Leviathan field by 2019 with Noble Energy’s and Delek Group’s commitment to invest $1.5 billion over the next two years.

The Israeli Supreme Court’s March 27, 2016 decision that the parliamentary approved framework gas deal struck between the government and Noble/Delek partners in Israel’s Leviathan field is illegal on the basis that its central piece, the stability clause, is unconstitutional has shaken up Israel’s energy sector.[9] The reason is that if investing companies are forced to disengage, the possibility of developing Leviathan will be jeopardized for the coming years. Equal important, the resulting delays in progress on proposed supply projects between Israel and neighboring countries can damage the former's standing and credibility as a reliable supplier of gas resources. Thus, there is urgent need for a policy solution based on considerations that Israel cannot have a truly competitive market as there are two main fields and one meaningful buyer, which is the Israeli Electric Corporation. Practically, a policy solution can satisfy the terms of Israel’s anti-trust legislation which allows exemptions from limitations when a sector is viewed to have a natural monopoly.

By all means, regulatory stability is deemed significant for investors who currently stand on a fine line between staying or leaving the Israeli energy market, and eye benefits and risks in the post-sanctions Iranian opening of a large gas sector.

Cyprus Changes Tides for Natural Gas

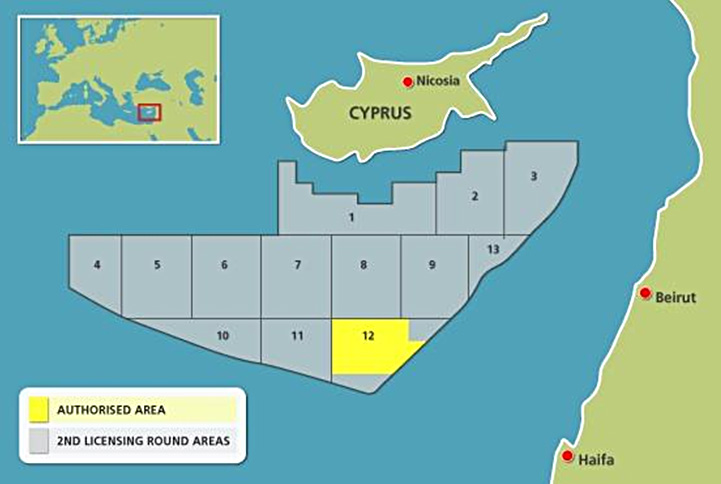

Another significant player for regional energy cooperation is Cyprus given that gas discoveries can turn the island into a net natural gas exporter. The recent declaration of commerciality for the Aphrodite gas field by its partners confirms the existence of substantial recoverable natural gas reserves in Block 12 of Cyprus’ Exclusive Economic Zone (EEZ).[10] Commerciality of Aphrodite field presents a milestone to Cyprus’ transition from the stage of hydrocarbons exploration to that of exploitation, and a significant step towards the monetization of the island’s indigenous natural gas reserves, both for domestic use as well as exports.

Cyprus has already signed a Memorandum of Understanding with Egypt on gas cooperation for the downstream exploitation of output from the Aphrodite field by utilizing gas infrastructure existing in the Arab country via a direct subsea pipeline. Additionally, the inauguration of a tripartite partnership between Cyprus, Egypt and Greece with the signing of the Cairo declaration in November 2014 falls on maritime security and energy cooperation, and is currently reinforced by high level political and technical meetings.[11] The Greek dimension in the partnership is important because of Greece’s strategic location at the crossroads of Europe, Asia and Africa that can cuddle Cyprus-Egypt as well as Israel energy cooperation by linking gas pipelines away from war risk zones.

Figure 2: Offshore Cyprus hydrocarbons exploration blocks

In monetizing natural gas resources, Cyprus also needs to face a prime challenge associated with one of the multiple regional export options that are on the table, which is the pipeline project that would connect Israel’s Leviathan field to the Turkish coast. For the Cypriot side, the prerequisite to this export option is the resolution of the Cyprus conflict since the pipeline would have to cross Cyprus’s EEZ. There is growing consent that the natural gas discoveries in Cyprus could prove a catalyst for a breakthrough in the strategic impasse over the island, which is still divided between Greek-Cypriot and Turkish-Cypriot communities.

It is in any case noticeable that a vote of confidence related to the island’s regional energy standing is conceded by major oilfield services companies, such as Halliburton and Schlumberger that have based operations for the East Mediterranean in Cyprus.[12]

No doubt that Cyprus’s natural gas discoveries present a game changer that poses all kinds of risks and opportunities for the island’s economic recovery and growth. It is in this context that policies need to center on the creation of a Cypriot sovereign wealth fund, preferably based on the Norwegian model, to recycle revenues, and the establishment of a regional sponsor-supported non-governmental organization or council that would include energy companies, energy industry service providers, energy industry associations, and other related stakeholders in the region. Once established, the council could seek government participation from the littoral states of the Eastern Mediterranean. It could then become a point of reference and also an avenue of communication between governments and industry, as well as a clearinghouse for ideas and plans for mutually beneficial energy development in the region.

Greece’s Challenge for Exploration and Production: What Lies Ahead

Development of Greece’s energy reserves will likely be further delayed unless key challenges are addressed. These challenges include domestic political instability, the high cost of exploration and drilling, the prolongation of the Exclusive Economic Zone (EEZ) delimitation problems with neighboring Turkey, and cheap electricity prices imposed by the state-monopoly of the Public Power Corporation.

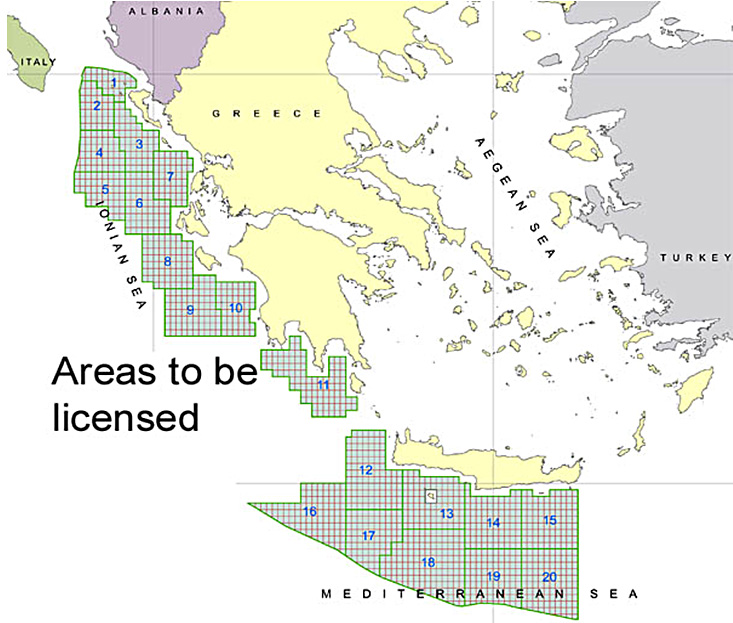

It is important to highlight the value of Greece as a transit country for regional gas supplies to Europe, especially given the lengthy process of exploration and development of major energy projects that are expected to increase economic growth, job creation and competitiveness. The Trans Adriatic Pipeline (TAP) route for example will run through 13 provinces in Northern Greece and is expected to create 10,000 direct and indirect jobs, even though approval was delayed to mid-January 2016 due to objections from environmental groups and local communities.[13] Despite the belief that oil and gas exploration and production (E&P) could help mediate the economic crisis, the Greek government has proceeded with only three concessions, delaying the approval of licenses and permits. Specifically, bids for the onshore licensing round of areas in Southern and Western Greece are currently under evaluation, as is the second international licensing round, whose deadline expired in July 2014. Prerequisites for attracting international companies in Greek gas E&P include resolving the Greek political decision-making standoff; the approval of a new regulatory framework for the gas sector; and the appointment of specialized personnel at the Greek Hydrocarbon Management Company (EDEY) to speed tender procedures.

Figure 3: Exploration blocks along Western and Southern Greece

Energean Oil and Gas company, Greece’s only hydrocarbon producer, has initiated a $200 million investment plan for 2015-2018, which is aimed at raising production to 10,000 barrels per day by the end of 2017.[14] This is a significant increase from today’s 3,000 at the Prinos basin in the north Aegean Sea. In the context of Israel-Cyprus-Greece synergies, Energean considers Israel a key country and thereby has taken the decision to commit to offshore Israel through the joint Ocean/Energean deep-sea operator even if that means that the Greek company will be excluded from Iran.

The Security of Mediterranean Oil and Gas Infrastructure

Security needs to be prioritized in the Eastern Mediterranean. Terrorism, human trafficking, and illegal migration pose major threats to the security of the oil and gas industry and thus require a collective regional response. A thorough examination of effective security measures finds that the Australian experience could be an efficient guide for the East Mediterranean. Australia is the world’s ninth largest energy producer, accounting for around 2.4 percent of world energy production, generating $28 billion in revenue annually, and contributing 58 percent of the country’s primary energy needs.[15] Australia’s experience has been utilized to improve the security framework of the oil and gas infrastructure in the Gulf of Mexico.

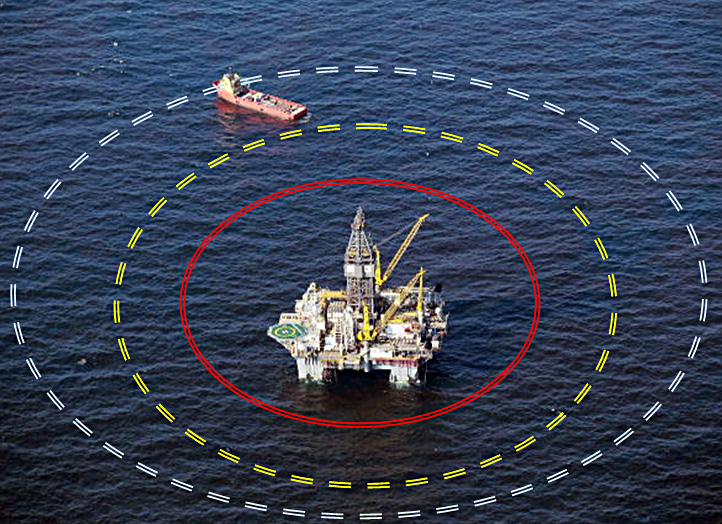

Assessments indicate that terrorist threats to offshore infrastructure could emanate from home-grown or internationally driven terrorist operations.[16] Thus consideration has to be given both to extending and hardening current security exclusion zone boundaries and to increasing the safety and security of offshore facilities from unlawful or unauthorized intrusion and threat. Recommendations focus on the introduction of a three-tiered approach to security zoning for all offshore facilities: 1) a cautionary zone of 15 nautical miles; 2) an area to be avoided of 5 nautical miles; and 3) an exclusion zone between 1 and 2.5 nautical miles, with approval to enter granted only by the facilities’ operator.[17]

Figure 4: Security zoning for offshore oil and gas facilities

Physical Threats to East Mediterranean Energy Supply have to be approached in terms of:

Pipeline security:

Most oil and natural gas pipelines run above-ground and extend over hundreds of miles, making them highly visible and difficult to protect. Pipelines are prime symbolic targets, seen as representing foreign influence & economic or political inequality.

For example, politically motivated groups have attacked oil pipelines in Colombia and Nigeria, while since 2011 Arish Askelon gas pipeline from Egypt to Israel and Jordan has been repeatedly blowed up.

In terms of:

Maritime Security:

Oil and LNG tankers are slow moving and rarely well-defended. Offshore platforms and ports are vulnerable. Global shipping lanes pass through narrow channels known as chokepoints could be targets (such as the Strait of Hormuz and the Bosporus Straits). Attack on, or interdiction of, a vessel in chokepoints could result in closures or limits on traffic, and thus would seriously impact world energy supply.

Evidently, the Mediterranean oil and gas fields must be protected by a combination of local state security forces and company operators’ private security forces. So regional countries like Israel, Cyprus, Egypt, Greece, Jordan, Turkey and others could partner to analyze risks and find solutions based either on prevention and detection or response and recovery.

Conclusion

No doubt that the East Mediterranean gas discoveries provide a golden opportunity for energy security and cooperation, an opportunity that must not be neglected because as it is aptly highlighted in a famous Arabian proverb “three things come not back; the spoken word, the sped arrow, and the neglected opportunity”. It is in this spirit that regional countries coordinate policies and share best practices so that the opportunity is not neglected.

References

1. Charles, E. The Impact of Israel’s High Court Gas Decision, Cyprus Mail (English News Outlet), May 3rd, 2016

2. European Commisssion. In the Mediterranean, the Adriatic and the Ionian, Report 4, September 2014

3. Eran, O. Active Israeli Policy in the Mediterranean Basin, INSS Insight No. 775, December 6, 2015

4. Lerman, E. Israel’s Emerging Relations in the Eastern Mediterranean, BESA Center Perspectives Paper No. 321, November 8, 2015

5. El-Katiri, L. and El-Katiri, M. Regionalizing East Mediterranean Gas: Energy Security, Stability and the US Role, Strategic Studies Institute and US Army War College Press, December 2014

6. Keinon, H. Analysis: Using Israel’s Gas to Cement Ties, Jerusalem Post (Israeli Daily), Janyary 29, 2016

7. Egypt Oil Gas Industry Analysis and Forecast Report (Q1 2016), Suppl\y, Demand, Investments, Competition and Projects to 2025, Published by Research and Markets: San Fransisco, February 2016

8. Henderson, S. and Schenker, D. Jordan’s Energy Decision: Go with Israel, Policy Alert: Washington Institute for Near Easr Policy, September 3, 2014.

9. Mediterranean Energy Regulators, Interconnetion Infrastructures in the Mediterranean: A Challenging Environment for Investments, Med 15 - 19 GA, Italy, 2015

10. Konofagos, E. and Karageorgis, K. East Mediterranean Gas Discoveries: Offshore Security Challenges and "The Greek Case", Hellenic Naval Academy, 2014

11. Nathanson, R. and Levy, R. Natural Gas in the Eastern Mediterranean Casus Belli or Chance for Regional Cooperation? (ed). IEPN and INNS, Israel, November 2012

12. Wurmser, D. The Geopolitics of Israel’s Offshore Gas Reserves, Center for Geopolitical Analysis, April 4, 2013

13. Giannakopoulos, A. Energy Cooperation and Security in the Eastern Mediterranean: A Seismic Shift towards Peace or Conflict? (ed.), The S. Daniel Abraham Center for International and Regional Studies, Research Paper No. 8 February 2016

[1] Antonia Dimou is diplomatic advisor at the Hellenic Parliament; senior RIEAS advisor; associate at the Center for Strategic Studies, University of Jordan; fellow at the Center for Middle East Development University of California, Los Angeles; and, instructor at Webster Athens.

[2] Jeffrey Kupfer, «The Link between Israel and America’s Natural Gas Boom”, Fortune (Electronic Magazine), December 12, 2014

[3] Noble Energy, “Noble Energy Announces Agreement to Sell Tamar Gas to Multiple Customers in Jordan”, February 19, 2014. Accessed at: http://investors.nobleenergyinc.com/releasedetail.cfm?ReleaseID=826568

[4] Reuters, “Israel Gas Field Partners Sign LOI on Exports to Egypt LNG Plants”, May 6, 2014

[5] Matthew Bryza, “Build a Turkey-Israel Pipeline to Bring Stability”, The Japan Times (English Daily), January 26, 2014

[6] Sharon Udasin, “Palestinian Power Company Nixing Leviathan Gas Import Deal”, Jerusalem Post (Israeli Daily), November 3rd, 2015.

[7] “Leviathan Field Monopoly is Focus of Israel’s Anti-Trust Regulator”, Oil & Gas 360, Janhuary 5, 2015. Accessed at: http://www.oilandgas360.com/leviathan-field-monopoly-focus-israels-anti-trust-regulator/

[8] Moti Bassok and Avi Bar-Eli, “Israel, Cartel Reach Accord on Regulating Natural Gas Industry”, Haaretz (Israeli Daily), August 13, 2015

[9] Orr Hirschauge and Rory Jones, “Israel’s Supreme Court Rules Against Offshore Gas Deal”, The Wall Street Journal, March 27, 2016.

[10] Cyprus Mail, “Aphrodite Gas Field Declared Commercial”, June 7, 2015. Accessed at: http://cyprus-mail.com/2015/06/07/aphrodite-gas-field-declared-commercial/

[11] Karen Ayat, “Egypt, Greece and Cyprus Pledge Energy Cooperation”, Natural Gas Europe, November 10, 2014.

[12] Elias Hazou, “Oilfield Services Leaders to Set Up Regional Base in Cyprus”, Cyprus Mail, May 28, 2014.

[13] European Commission (Press release), “State Aid: Commission Approves Agreement between Greece and TAP Allowing New Gas Pipeline to Enter Europe”, Brussels, 3 March 2016.

[14] Reuters, “Greek Fledgling Oil Sector Steps Up Production”, January 7, 2016. Accessed at: http://af.reuters.com/article/commoditiesNews/idAFL8N14R2FD20160107

[15] Parliament of Australia, Migration Amendment (Offshore Resources Activity) Repeal Bill 2014; Second Reading. Accessed at: http://www.aph.gov.au/Parliamentary_Business/Hansard/Hansard_Display?bid=chamber/hansardr/6f011bde-9138-44d1-93a9-08f7c4113f58/&sid=0190

[16] Assaf Harel, ‘Preventing Terrorist Attacks on Offshore Platforms: Do States Have Sufficient Legal Tools?’, Harvard National Security Journal, Vol. 4, No. 1, 2013.

[17] Mikhail Kashubsky and Anthony Morrison, Security of Offshore Oil and Gas Facilities: Exclusion Zones and Ships’ Routeing, Australian Journal of Maritime and Ocean Affairs, Vol. 5(1), 2013.